January 2021

The pandemic has altered the lives of every American. Despite buoyant markets, millions of Americans faced unprecedented financial hardship caused by COVID-19. It has upended what work, income, and employment opportunities look like, as well as retirement. It has eaten into savings, forced people into debt, and created unprecedented levels of housing instability. And while the rollout of vaccinations gives some hope, continued lockdowns coupled with the change of power in Washington and current political unrest are causing many to continue feeling uncertain about the future. Yet certain populations, including seniors, people of color, and lower income Americans, have been disproportionately impacted both by the virus itself and the instability in its wake.

The SimplyWise Retirement Confidence Index, running since May 2020, tracks evolving American confidence around savings and retirement. The latest Index polled 1,029 citizens ages 18+ between January 8-10, 2021, and found that concerns over retirement finances and savings remain high—yet vary considerably across income, race, gender, and even political party. The survey explored how citizens are approaching savings, Social Security, and retirement, especially given the recent election and worsening situation around COVID-19.

Key Findings

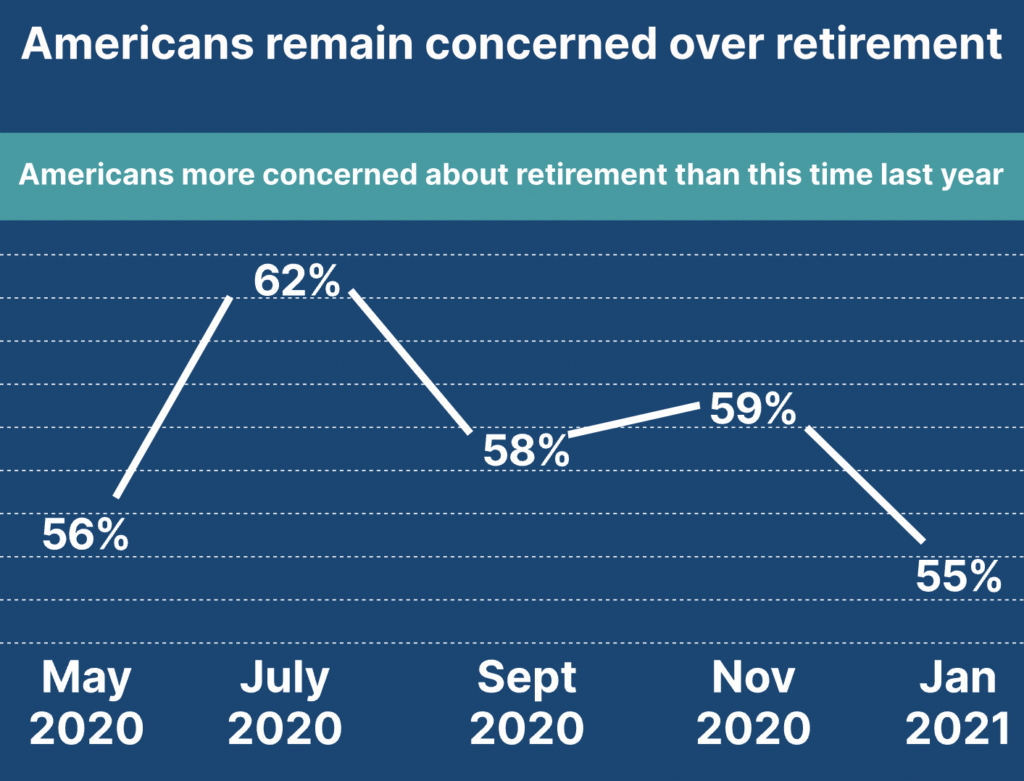

- 55% of people are more concerned about retirement today than this time last year.

- 44% of Americans worry they’ll never be able to retire—an all-time high.

- 69% of Social Security beneficiaries experienced at least 1 scam attempt in the last 3 months.

- 23% of Americans don’t have any kind of retirement plan.

- 51% of Americans will need a 3rd stimulus check within the next 3 months.

- 64% of Black Americans could not last more than 3 months off their savings, compared to 48% of White Americans.

- 25% of Americans in their 60s could not last more than 3 months off their savings—an all-time high.

- 75% of people who were laid off due to COVID-19 couldn’t come up with $500 cash.

- 45% of Black Americans now fear falling behind on their rent or mortgage, as compared to 44% of Hispanic Americans, and 28% of White Americans.

Disparity in American retirement outlook

The SimplyWise Retirement Confidence Index has found since its inception in May 2020 that retirement confidence remains low. The January Index found that 55% of people are more concerned about retirement today than this time last year. This is compared to last year’s 56% in May, 62% in July, 58% in September, and 59% in November.

That means that concern over retirement is now at the lowest point since the pandemic began. These results reflect a somewhat more optimistic view of the future. While a majority of Americans do continue to feel financially squeezed today, as 2021 begins, many appear to have a brighter outlook.

However, simply looking at the average retirement confidence level does not paint the full picture in 2021. Deep disparities loom within the data. The January Index found that Black Americans continue to be the most concerned about retirement; 59% reported they are more concerned about their retirement prospects today compared to this time last year. That is compared to 57% of Hispanic Americans and 54% of White and Asian Americans who said they are more concerned.

It also varied by income bracket. The January Index found that 58% of Americans with a household income of $50,000 or less are more concerned about retirement today compared to this time last year. This is compared to just 40% of Americans with a household income of $150,000 or above who are more concerned about retirement today.

Yet the greatest concern for the future was, understandably, among those who have been laid off or furloughed during the COVID-19 pandemic. Of people making the same income they did prior to the pandemic, 52% feel more concerned about retirement today. By comparison, 69% of workers whose income has been lost or reduced due to the pandemic are now more concerned about retirement.

For people not yet claiming Social Security benefits, financial concerns remain among the highest anxieties in thinking about retirement. As each of our previous indices found, the number one fear of Americans for retirement is that Social Security will end. The January Index found that for those not yet claiming Social Security retirement benefits, 53% fear those benefits will dry up. That anxiety was most acute for people in their 50s, nearest to their legal retiring age. Of that group, 58% worry about Social Security drying up during their lifetime.

For this reason, many believe they will be working for their whole lives. In fact, the January Index saw that more people than ever today worry they will never be able to retire. For those not yet claiming Social Security retirement, 44% worry they will never retire.

Interestingly, when the same question was asked to Americans in their 50s as well as seniors (age 60+), the numbers had also increased. While the previous SimplyWise surveys (from May 2020 onwards) found approximately one in three in their 50s worry about not being able to retire, the January poll found that 42% worry they may never be able to retire. Perhaps worse, for seniors, many of whom are already retired from work, a total 18% believe they never will retire. That is almost one in five American seniors who fear they may have to work for the rest of their life.

The January survey found that other major retirement concerns for Americans not yet collecting Social Security retirement benefits were specifically around savings and expenses. The January 2021 Index found that 49% worry they will outlive their savings, and 42% worry about covering daily living expenses when they retire. Another 47% are concerned about their ability to cover medical bills in retirement. And for people in their 50s, 53% worry about paying medical bills in retirement—an Index-high.

In fact, only half are confident that they will be able to maintain the same quality of life they enjoy today once they retire. That number varies greatly by age. According to the January Index, 61% of Americans in their 20s believe they will be able to enjoy their same quality of life in retirement. This is compared to 53% of people in their 30s and 47% of people in their 40s and 50s who believe their life quality will not change after retiring.

Most Americans to work in retirement

The pandemic continues to impact the savings, finances, and employment of Americans—and this is particularly disruptive for people nearing retirement age (and who are dealing with the most threat from scams and targeted fraud on their bank/credit card accounts). Many have lost employment, or are having to weigh health risks of going back into a workplace to return to work.

Given this current climate, 9% of people in their 50s and 60s are now considering retiring earlier than planned. Many of them will be claiming their Social Security benefits earlier than expected. Of course, claiming benefits before retirement age permanently reduces what you could receive monthly from Social Security. In fact, the January Index found that 10% of people in their 50s and 60s are now considering claiming Social Security benefits early.

However, many more are considering postponing retirement today. An Index-high of 32% of people in their 50s are now planning to postpone retirement from work. And a record 21% of people in their 60s are now planning to postpone retirement from work.

Those plans may be attributed to the fact that only 63% of workers in their 50s and 60s are making the same income they did prior to the pandemic. The Index also found that 20% of workers in their 50s and 60s have maintained their jobs but had their income reduced during the pandemic.

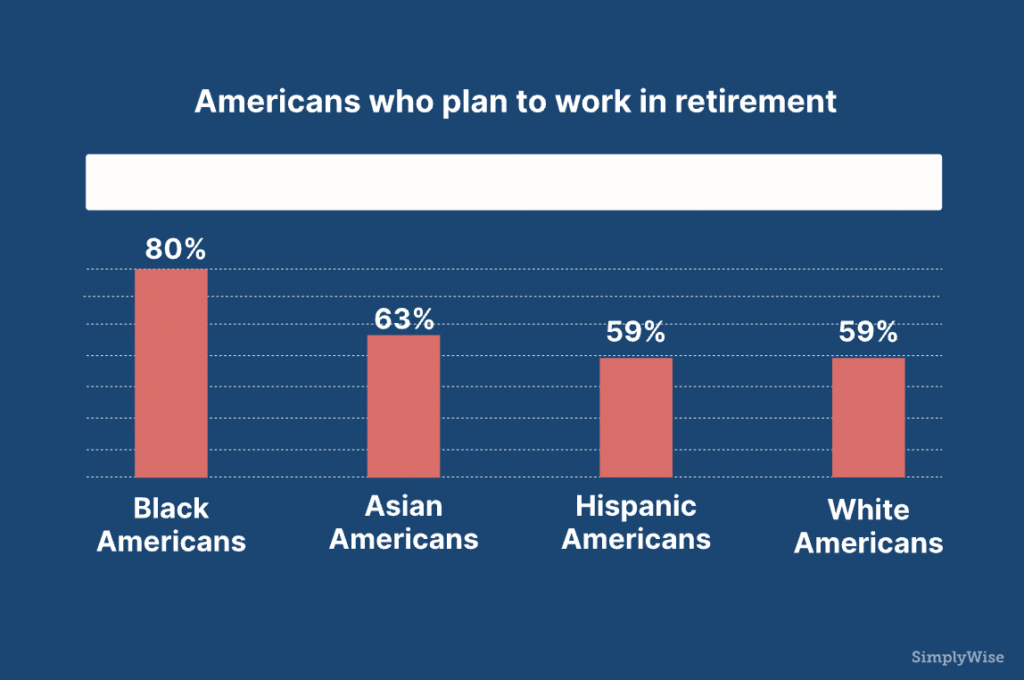

Yet for a majority of Americans today, “retiring” no longer means the end of. The January Index found that 71% of workers plan to continue working in retirement. That is compared to 74% of workers back in November who said they plan to work after claiming Social Security retirement benefits. Previous 2020 results were similar: 67% in May, 72% in July, and 73% in September reported plans to work in “retirement”.

There was a racial disparity in plans to work in retirement. In fact, 80% of Black Americans reported that they plan to work after claiming Social Security benefits. This is an Index high. It is compared to 63% of Asian Americans and 59% of Hispanic and White Americans who reported they plan to work in retirement.

For people nearest to retiring age, those in their 50s, the numbers were lower than the national average—though not by much. The January survey found that 59% of people in their 50s now plan to work in retirement. That is split between 42% who plan to work part-time and 17% who plan to work full-time after claiming Social Security retirement benefits. That 17% is compared to the May 2020 Index results, which found that just 8% of people in their 50s planned to work full time in “retirement”.

Again, this may be yet another indicator of financial planning anxieties for retirement, particularly for those nearing retiring age. Nonetheless, it does highlight the fact that many do in fact count on having work income into their 60s or 70s. This reliance on work income for one’s finances later in life, however, can be harmful. Health problems or unexpected job losses (like many Americans are facing today) can force people out of work and into early retirement. Wherever possible, building up alternative assets and savings can be critical for retirement.

Disparity in American savings

Since the start of the Retirement Confidence Index in May 2020, the numbers around annual retirement savings have remained consistent. In line with the previous surveys, the January Index found that 32% of Americans saved $0 for retirement in the last year. That means that almost one third of Americans saved nothing for retirement in 2020. The Index also found that 23% of Americans don’t have any retirement plan at all.

There was a gender divide in the January results. Again, men saved more than women across the board. For example, 63% of men versus 47% of women saved $500 or more for retirement in the last year. Moreover, just 26% of men saved $0 for retirement in 2020, compared to 36% of women.

There was also a disparity when it came to those who have been laid off or furloughed due to COVID-19. Of that group, 45% saved $0 for retirement in 2020.

Interestingly, when narrowing in on savings of the 50-59 age group, the results looked similar to that of the average American. In fact, 31% of people in their 50s saved nothing for retirement in 2020. And 45% saved under $1,000 for retirement over the year. But this data is troubling, given that financial advisors recommend saving the most for retirement in your 50s and early 60s. This is because of policy that allows for a “catch up” period for those 50 years or older to contribute beyond their retirement account’s usual annual contribution limit. However, the recent survey found that of Americans in their 50s, 27% saved $0 for retirement in the last year. And 42% could not last more than a month off their savings.

There is a bright spot with regards to savings, however. Across the board, Americans do feel more determined to improve their savings in the new year. In fact, 54% of the country said they plan to save more for retirement in 2021. Of people in their 50s, 55% plan to save more for retirement this year.

Beyond retirement savings, the overall financial and savings reality for many Americans today remains grim. When asked how long they could afford to not work and live off their savings, 37% of all Americans could not last a month. Fifty-eight percent of all Americans could not live off their savings for more than 3 months.

Like with retirement savings, there was a gender and racial divide in overall savings. Twenty-eight percent of men, versus 45% of women, could not last a month off their savings. For Hispanic and Black Americans, 47% and 46% respectively could not last a month on their savings. That is compared to 36% of White and 30% of Asian Americans.

The numbers were also alarming when it came to older Americans, many of whom are already retired. For example, 25% of Americans in their 60s said they could not last more than a month off their savings—an Index-high.

Finally, there was also a disparity when it came to those who have been laid off or furloughed due to COVID-19. A full 47% of them could not last a month off of their savings. And 25% could not last even two weeks off their savings.

The findings highlight the urgency of COVID-relief legislation for many Americans. In fact, the January Index found that over half of Americans (51%) say they will need a third stimulus check in the next three months. And 28% of Americans say they will need another check in just one month. The numbers were much more dramatic when it came to those who have lost their job due to the COVID-19 pandemic. For those unemployed Americans, 76% say they will need another stimulus check within the next three months.

Economic insecurity and disparity intensified by pandemic

Despite some rebounding employment and savings numbers today, the reality for many Americans is that incomes and savings have been hit hard in the last year. Of course, even before the pandemic, most Americans were living paycheck to paycheck. Yet the pandemic has in many ways intensified class and racial divisions. SimplyWise’s January survey found that an Index-high of 52% of Americans would not be able to come up with $500 cash right now without selling something or taking out a loan. This is up from 43% reported in November 2020 who could not come up with $500 cash.

That response varies greatly across racial lines as well as current employment status. While 45% of White Americans cannot come up with $500 cash, 67% of Black and 66% of Hispanic Americans could not come up with that money without selling something or taking out a loan. And an unbelievable 75% of people who were laid off due to COVID-19 could not come up with $500 cash today.

With incomes hit hard by the pandemic and no savings to fall back on, many Americans are concerned what this means for where they live in the coming year. In fact, the survey found that 60% have some concern over their housing right now. Though again, there was a serious racial disparity in this data. Over 46% of White Americans report that they ‘don’t have any concerns with regards to their housing’. That is compared to 26% of Black Americans and 23% of Hispanic Americans who ‘don’t have concerns’ about their housing.

The survey also found that a total of one in three Americans worries about falling behind on their rent or mortgage. Yet those numbers are more dramatic for people of color. In fact, 45% of Black Americans fear falling behind on their rent or mortgage, compared to 44% of Hispanic Americans, and 28% of White Americans.

Another one in ten Americans worries they will have to sell their home this year. Another 9% worry they will have to move into a more affordable home. And a distressing 8% of Americans worry about being evicted from their home.

For this reason, many Americans are looking to other assets to pay the bills right now. This is especially true for older Americans. For example, 11% of people in their 50s and 9% of people in their 60s are planning to withdraw from emergency savings today to pay the bills. For Social Security beneficiaries, many of whom depend on a fixed income, 14% are now considering selling their home given the economic climate. Another 14% of beneficiaries are planning to refinance their home. And 18% of beneficiaries are planning to withdraw from emergency savings for cash.

In 2020, a number of Americans tapped their retirement accounts for cash. This was due to a part of the CARES Act that waived the usual 10% penalty on retirement account withdrawals up to $100,000 for distributions made throughout 2020. (Typically, withdrawing from a reitmrenet account before age 59 ½ results in a 10% penalty on the amount taken.) According to the policy, as long as the withdrawn amounts were repaid to the retirement plan within a three-year window, the funds would be tax-free. Distributions not repaid would become taxable income which could be taxed ratably over three years.

Yet many Americans are not able or willing to pay back the withdrawn funds into their retirement accounts. In fact, the January Index found that of people who took the CARES Act withdrawal from their retirement plan in 2020, 43% do not plan to pay it back (57% do plan to pay it back). Of people laid off due to COVID-19 who took a CARES Act withdrawal, 52% are not planning to pay it back.

Unfortunately, many Americans who would have been eligible did not even know they had the option to tap these accounts for funds. The January Index found that 34% of people who have a retirement plan were not aware that the CARES Act policy made retirement withdrawals penalty-free.

Congress did not extend this 2020 policy, so Americans are no longer able to withdraw penalty-free from these accounts in 2021. However, the January Index did find that 21% of Americans are still planning to withdraw from their 401(k) during 2021, despite the return of the withdrawal penalty. It may be the best alternative those citizens have today.

Indeed, with the growing coronavirus case numbers, the recent political turmoil, and the upcoming presidential inauguration, the short-term outlook feels uncertain for a number of Americans. The January Index found that 37% believe the economy will get better in the next six months—and just 28% believe it will get better. However, there was a divide along party lines. Of Democrats, 37% believe the economy will get better, where just 16% of Republicans believe it will get better.

Future of Social Security feels uncertain

Today’s macroeconomic and sociopolitical uncertainty, including the upcoming transfer of power in Washington D.C., spills over into concern for the future of government programs. This is especially true for the Social Security Administration (SSA), which has long suffered a funding shortfall.

In fact, even before COVID-19 wracked the country, the SSA’s Board of Trustees announced in early 2020 that Social Security’s funds would be exhausted by 2035. Note that this did not signify the end of the program. Rather, it was a warning that its cash reserves would be depleted, and citizens’ benefits would become fully dependent on taxes collected from workers each year. The Board of Trustees reported that this would mean beneficiaries were paid only 79% of the money they were owed.

However, the pandemic has accelerated the exhaustion of the program’s cash reserves. This is because the payroll taxes that fund the SSA’s coffers were cut into when unemployment sunk to record levels in 2020. The destiny of the program now lies both in the hands of legislators as well as the prolongation of unemployment numbers.

Moreover, 2020 was a highly disruptive year for current Social Security beneficiaries in receiving their benefits. Starting in March 2020, local Social Security offices closed due to COVID-19 to protect employees as well as the vulnerable populations they serve. With the confusion around the office closures and changing communication methods with the SSA, Social Security-related scams then escalated over the year.

Indeed, the January 2021 Index found that 46% of Americans have experienced at least one attempted Social Security scam in the last three months. That is exactly in line with the November Index data, which found that 47% of Americans had experienced at least one such scam attempt. Further, the January Index found that an unbelievable 21% of Americans have experienced three or more attempted Social Security scams in that time. The data, however, was most shocking for current Social Security recipients, who regularly receive communications from Social Security. A full 69% of Social Security beneficiaries have experienced at least one Social Security scam attempt in the last three months.

Given the enduring impact of the pandemic, SimplyWise has collated resources to help current beneficiaries navigate the SSA amidst the uncertainty.

First, while offices are closed for most in-person visits (unless in the case of “dire need”), most are still answering phones. SimplyWise has a created a resource that breaks down, by state, the latest COVID-specific information for every local office:

- California Social Security offices

- Florida Social Security offices

- New York Social Security offices

- Texas Social Security offices

- Pennsylvania Social Security offices

- Find your local Social Security office here

Second, in order to protect against the increasing number of scams, and in particular Social Security scams out there today, it is critical to stay informed about the latest practices by fraudsters. SimplyWise compiles lists of recent scams as well as resources to protect against them. Learn more here.

Takeaways

Vulnerable groups, including seniors and people of color, have been disproportionately affected by the pandemic. In 2020, communities and governments around the country worked to offer relief for all those hit hard by the coronavirus. From mutual aid to unemployment benefits and Social Security, these programs have provided much needed resources and support to these vulnerable and minority populations. Yet many of these benefit programs and new government policies can be confusing to understand.

Navigating benefits eligibility requires educating yourself about evolving policies and legislation affecting what you are owed. You can use a benefits calculator to see what you could be eligible for, from spousal or survivor benefits to a senior companion or tax credits.

“While the world is changing fast and things feel somewhat uncertain, staying both informed and empathetic with yourself and those around you will ensure that your future planning stays on track,” says Sam Abbas, CEO, SimplyWise. Understanding your financial options can help you to find benefits, save smarter, and take control amidst today’s uncertainty.

Methodology

The January 2021 SimplyWise Retirement Confidence Index was conducted as an online, random sample survey of 1,029 Americans adults (age 18+). The survey was fielded January 8-10, 2021. It was intended to explore sentiment around savings, retirement, and Social Security given the COVID-19 pandemic and current economic and political uncertainty.

See results from previous Indices below: