Frequently Asked Questions

How much can you get from Social Security spousal benefits?

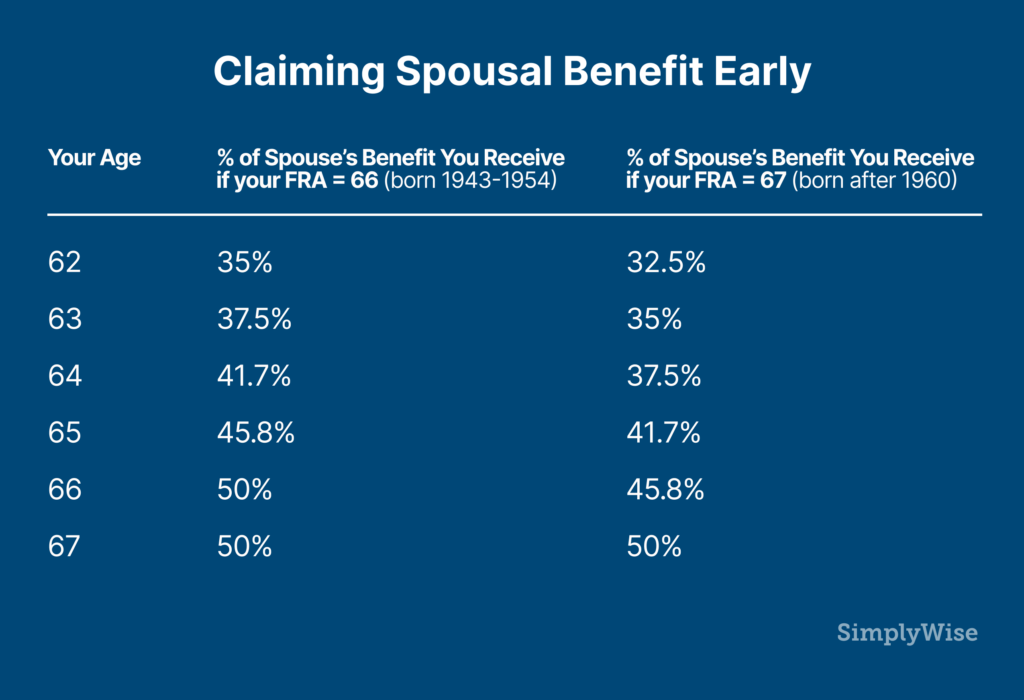

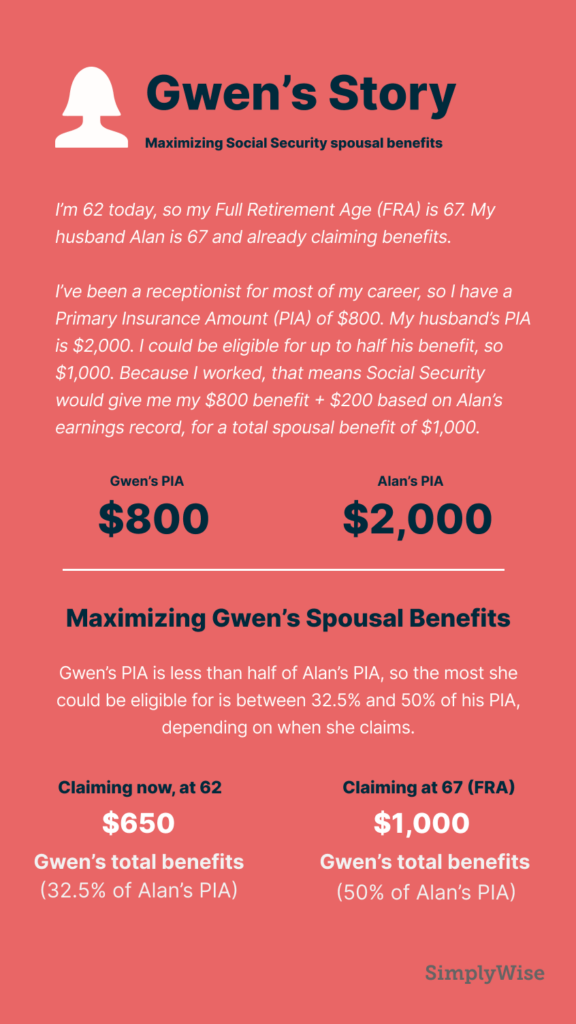

If you qualify, your spousal benefit can be up to 50% of your spouse or ex-spouse's primary insurance amount, which is the amount they are entitled to at their full retirement age. So if your spouse's primary insurance amount is $1,000, you could receive a maximum of $500 in spousal benefits. If you also qualify for your own retirement benefit, the two are not added together; you receive your own earned benefit plus an additional amount to bring you up to the higher spousal figure.

How much are spousal benefits reduced if you claim early?

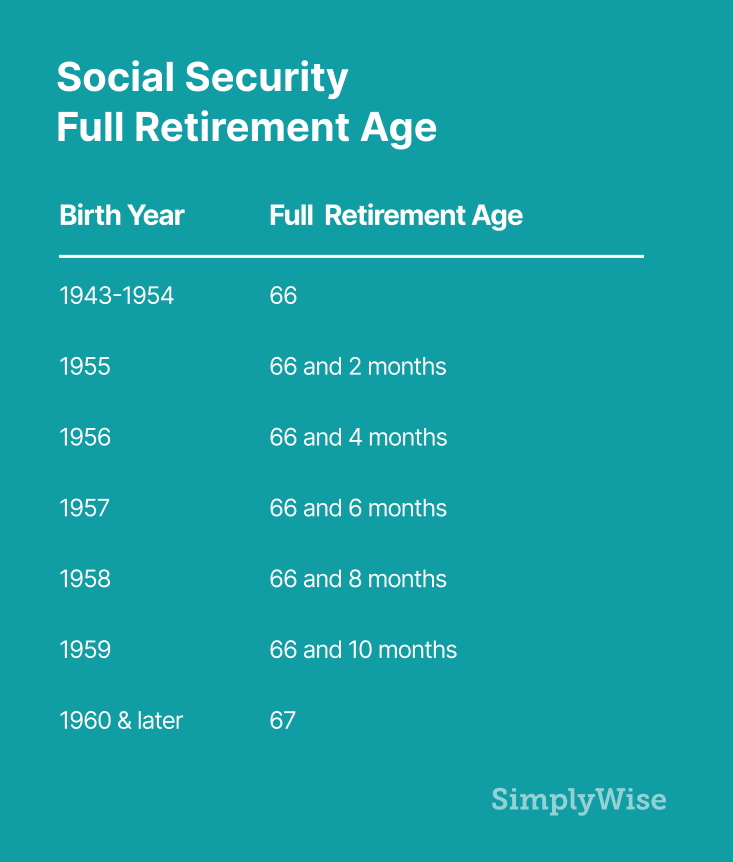

You are eligible to begin spousal benefits at age 62, but claiming before your full retirement age permanently reduces them. Spousal benefits are reduced by 25/36 of 1% for each month before your full retirement age, up to 36 months early, and benefits taken more than 36 months early are reduced an additional 5/12 of 1%. Unlike earned benefits, which grow between full retirement age and age 70, spousal benefits do not increase once you have reached full retirement age.

What is deemed filing and who does it apply to?

Deemed filing means that when you file for one benefit you must file for both your own earned benefit and your spousal benefit, and you receive only the higher of the two with no opportunity to switch later. The Bipartisan Budget Act of 2015 changed the rules so that anyone born on or after January 2, 1954 is subject to deemed filing even after reaching full retirement age. People born on January 1, 1954 or earlier can still file a restricted application for just one benefit until they reach full retirement age.