Introduction

Americans have always struggled to save. Many live paycheck to paycheck, on the very edge of financial security. Historically, that savings shortfall has been all the more dramatic when it comes to saving for retirement.

But with the coronavirus pandemic and the havoc it has wrought on the economy, that retirement savings gap may worsen. Beyond the health impact, COVID-19 has created enormous economic uncertainty across the country. Market volatility has cut into retirement nest eggs for many; in the first three months of 2020, the average 401(k) dropped 20%. And a provision of the CARES Act that makes it easier to tap retirement accounts is likely to send those balances even lower in the months ahead.

Unemployment has skyrocketed to record highs, hitting 14.7% in April. That means that Social Security’s coffers (which are dependent on payroll taxes) are taking a hit. Moreover, the recent CARES Act allows companies to delay Social Security payouts for up to two years. And while this doesn’t affect current beneficiaries, it highlights the pandemic’s impact on the already increasing Social Security funding deficit. With all of this uncertainty, it’s not surprising that Americans are growing increasingly worried about their retirement prospects.

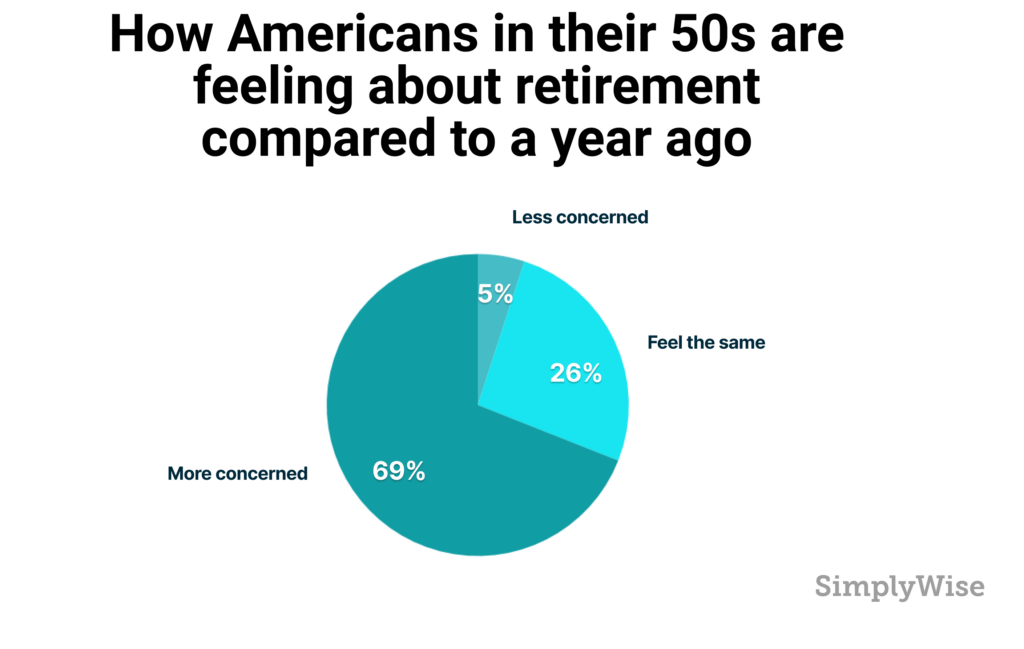

According to the May 2020 Simplywise Retirement Confidence Index, 56% of Americans are more concerned about retirement today compared to how they were feeling about it a year ago. The survey also found that 69% of people in their 50s—who are nearest to retirement—are more concerned about retirement today.

The study, which was conducted as an online, random sample survey of 1,070 Americans ages 18+ between May 8-9, 2020, explored how people are looking at retirement, Social Security, and savings today, particularly in light of the current crisis. We break down our findings, from changing rates of postponing retirement to how people are drawing from retirement savings during the pandemic.

Sections

Key Findings

Most Americans think Social Security will be dried up by the time they retire

The coronavirus impact on retirement savings

The gender impact on retirement savings

The coronavirus impact on Social Security claiming strategies

Americans are feeling squeezed across the board

Methodology

Key Findings

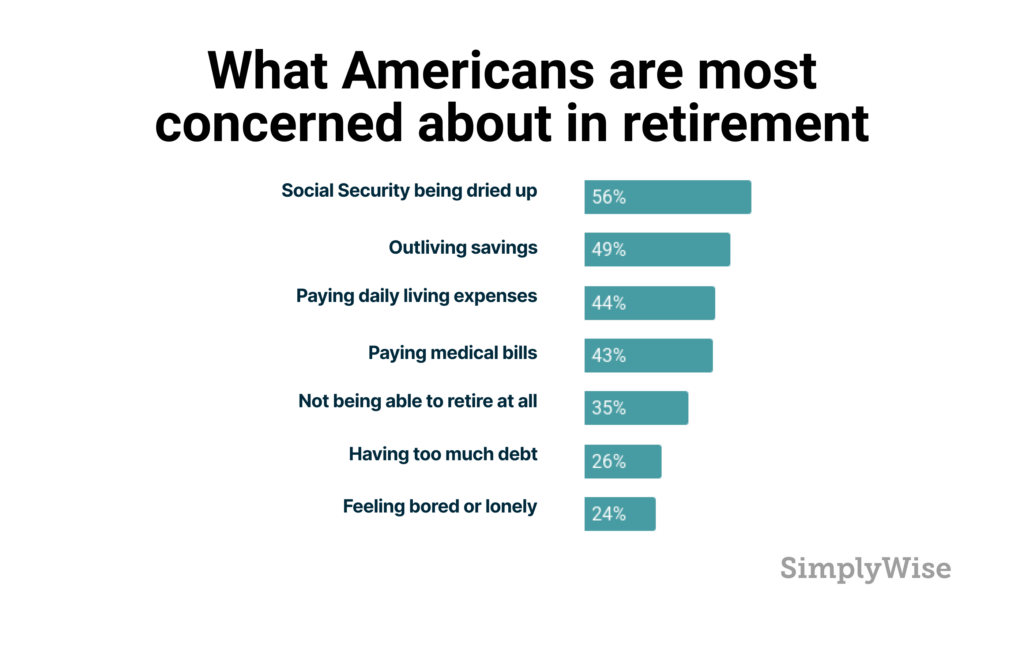

- The survey found that 56% of Americans more concerned about retirement today compared to a year ago. Main concerns include fear that the Social Security trust fund will dry up before or during retirement (which 56% believe) as well as outliving savings during retirement (which 49% believe is likely).

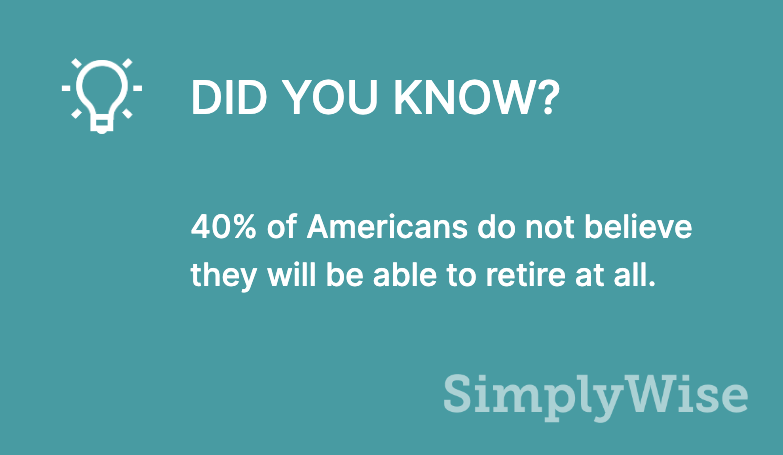

- 40% of workers are now concerned they won’t be able to retire at all.

- Over half of respondents believe their quality of life with suffer after claiming Social Security retirement benefits.

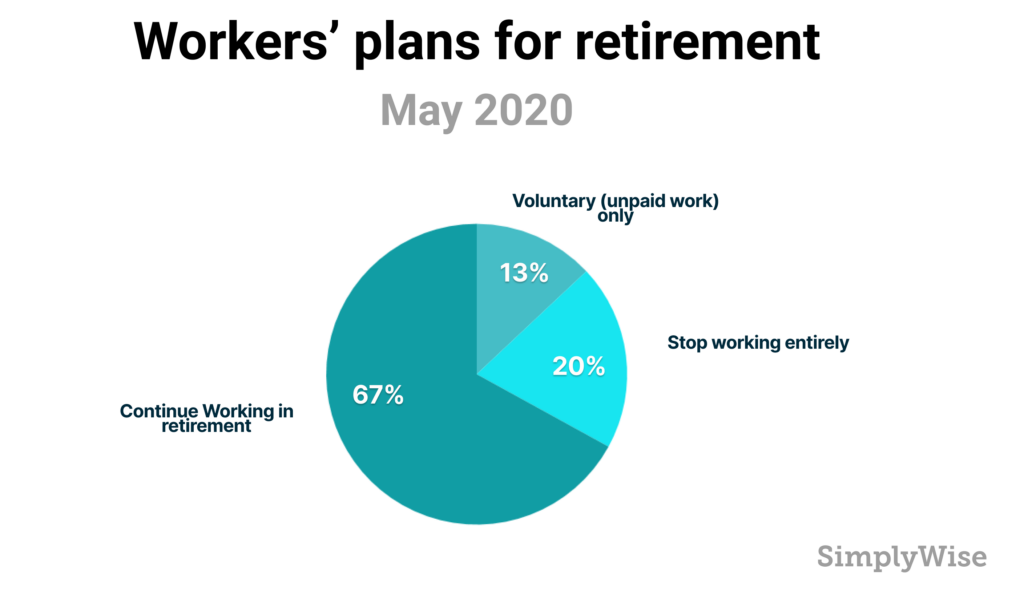

- 67% of working people plan to continue working in retirement.

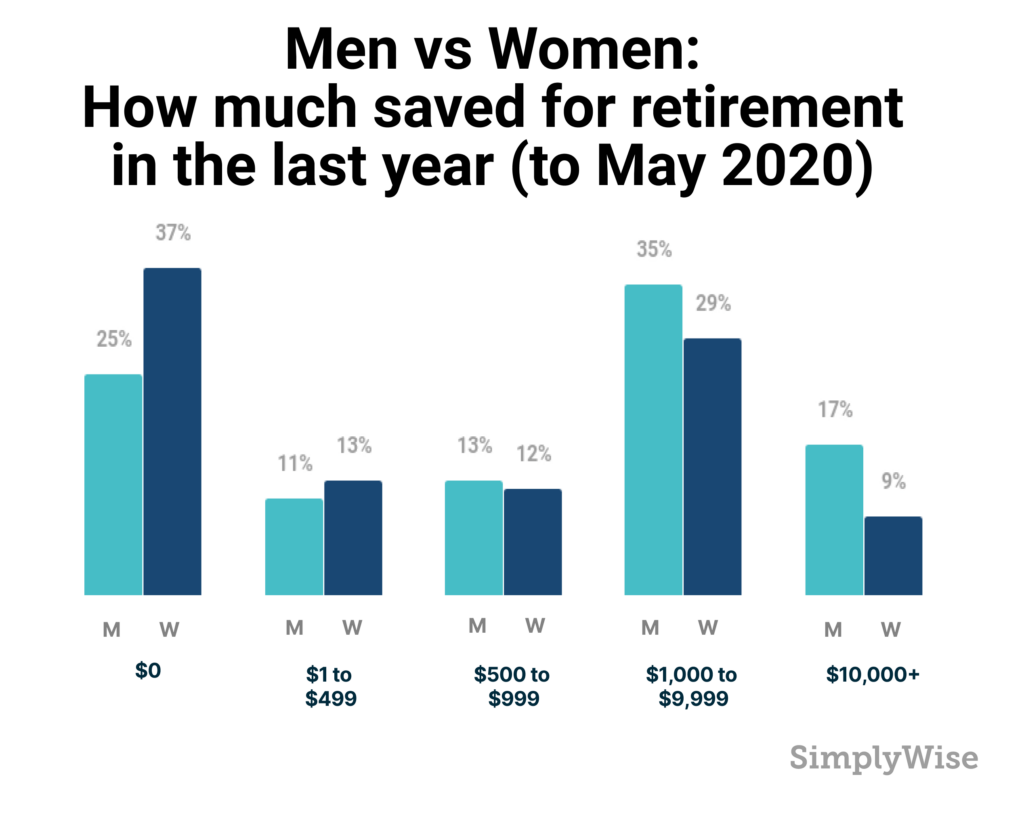

- One in three saved $0 for retirement in the last year. Women saved even less than men; 37% of women saved $0, and 50% saved under $500.

- One in five people believe it’s likely they will draw from 401(k) for cash right now, including 1 in 3 of those who have lost work.

- Given the current economic climate, 26% of respondents said they would postpone retirement altogether.

- Of respondents in their 50s and 60s, 33% are now planning to claim their Social Security retirement benefits early.

Most Americans think Social Security will be dried up by the time they retire

For those not yet claiming Social Security benefits, financial concerns are the greatest anxiety as they think about retirement.

An incredible 40% of workers from the Simplywise survey reported that they do not believe they will be able to retire at all. Half of respondents are concerned they will outlive their savings in retirement.

Paying everyday bills, particularly medical bills, is a great anxiety. Over 50% of people in their 50s reported being concerned about their ability to pay for medical and daily living expenses in retirement. Repaying lenders is another concern, with 28% concerned about having too much debit in retirement.

Over half of all respondents believe their quality of life will suffer after they begin collecting Social Security. For those not currently collecting retirement benefits, 58% believe those benefits won’t allow them to maintain the same quality of life they enjoy today. Looking at the average Social Security benefit—$1,503 per month in January of this year—it comes as no surprise. Especially given that, according to the U.S. Bureau of Labor Statistics, the average American spends $5,102 per month. Women were less confident than men that their savings and benefits would get them through retirement. Just 41% of women, compared to 55% of men, believed their retirement income would let them maintain their same lifestyle.

Indeed, the majority of respondents do not believe Social Security will cut it to pay their monthly expenses. On average, people answered that they expected Social Security to pay less than half of their monthly bills in retirement. What’s more, 56% of respondents not yet collecting benefits are concerned that Social Security will dry up altogether by the time they retire.

The concern is legitimate. According to the Social Security Board of Trustees, the trust funds responsible for disbursing benefits will be depleted by 2035. That does not mean Social Security will be gone altogether. But it does mean that its cash reserves will be gone, and it will only be able to dole out what it collects in taxes each year. If that happens, according to the Trustees, the Administration will only be able to pay beneficiaries 79% of the money they are owed. Its reserves are running out due to demographic trends. Generation X (the generation behind Baby Boomers) is much smaller, so while the Boomers swell the ranks of retirement beneficiaries, there are less workers paying in taxes to fund those benefits. This means current tax revenues won’t cover benefits and Social Security will have to tap the surplus. Add to that the current soaring unemployment numbers and it becomes hard for many to imagine what the future of Social Security looks like today.

Of course, even beyond financial concerns, there are other realities to face in entering the next phase of one’s life. Twenty five percent of respondents are worried about feeling bored or lonely once they retire. In fact, according to the U.S. Census Bureau, about one in five adults 65 to 74 years old lives alone. That figure doubles to around four in ten for those 85 and older. And while living alone does not necessarily result in social isolation, the reality is that with age, social contact does typically decrease. This can be due to factors like decreased health or mobility; family living far away; the death of friends or family members. And loneliness and isolation can actually have a deep impact on health and even finances for those in retirement. A study from AARP estimated that social isolation costs $6.7 billion to Medicare every year. The study found loneliness to be a risk factor in health conditions including arthritis, high blood pressure, heart disease, and diabetes.

The coronavirus impact on retirement savings

Given those financial concerns, one’s own savings and income is more important than ever to get through the supposedly “golden years”. And yet the act of saving, which is always challenging, has become even harder today with the crisis. One out of three respondents saved $0 for retirement in the last year. Of those recently furloughed or let go due to coronavirus, 50% have saved less than $500 for retirement in the last year, and 70% have saved less than $1000. For low to middle income individuals, the numbers were even worse. Over half of respondents whose annual income is below $50,000 saved $0 for retirement in the last year. And how could they? A 2017 study found that 78% of Americans live paycheck to paycheck. That means that for most citizens, there’s nothing leftover each month to put into long-term savings. (And this was was pre-pandemic and pre-employment crisis.)

In fact, according to the Bureau of Labor Statistics, for workers who are in the upper half of the country’s wage distribution (those earning a minimum of $36,000 on a full-time basis), 75% participate in a retirement plan. However, for workers in the bottom quarter of that salary distribution (whose salaries average $24,000), just 25% participate in a retirement plan.

The gender impact on retirement savings

The savings numbers for women—regardless of their working income level—looked similar to those of low and middle income individuals. And in fact, the same 2017 study found that women were most vulnerable, with 81% living paycheck to paycheck (compared with 75% of men). Perhaps for this reason, a whopping 37% of women (vs. 25% of men) saved nothing for retirement this past year—and exactly 50% of women saved less than $500 for retirement in the last year. Three in five women reported they are no longer confident they will be able to maintain their same quality of life in retirement. And 41% said they would not be able to come up with $500 in cash today.

This may be driven by the fact that on average, women earn less, work fewer years, and take less investment risk. Women make, on average, 85% of what their male counterparts do. They are also more likely than men to have part-time jobs. This renders them ineligible to participate in retirement savings plans. Women also continue to be more likely than their male counterparts to pause their careers for caregiving duties – both caring for children and, later in life, for aging family members. If they do return to work, they typically find it hard to make up the lost time in their earnings and savings. This translates to women having just 70% of what men have in overall retirement income.

The coronavirus impact on Social Security claiming strategies

The question is what all of this means for Americans who are nearing retiring age today. Some Americans are interpreting the current crisis as a call to postpone retirement. A full 26% of respondents said they would postpone stopping working altogether. Separately, people are also considering delaying retirement benefits. One in five (23%) respondents in their 50s and 60s are now planning to delay Social Security benefits.

In fact, there are important factors to weigh in considering when to claim. One’s monthly benefit from Social Security can considerably vary depending on the age chosen to start benefits. For example, if you claim your monthly benefit before your Full Retirement Age (and you can start claiming your Social Security benefits as early as 62), your monthly benefit will be lower. However, you will receive it for a longer period of time. If you claim your monthly benefit after reaching your Full Retirement Age, you’ll receive what is called “Delayed Retirement Credits”. DRCs translate to a much larger monthly check (though for a shorter period of time).

So the 23% of Americans making the decision today to delay retirement and stay in the workforce will claim higher amounts when they do collect. Specifically, their benefits will increase 8% for every year they wait.

Of course, even when one does officially retire and begin claiming benefits, that does not necessarily mean the end of work. Actually, the majority of Americans are planning to work throughout retirement today. Of those who are in the workforce today, 67% plan to continue working after claiming Social Security. There is no significant difference between gender in whether or not one works in retirement. For Americans recently laid off due to COVID-19, 73% are planning to work in retirement. And one in four of them actually changed their minds in the last year; after thinking they would not work during retirement, they now believe they will have to.

While it may not be what one imagined, working during retirement is not necessarily a bad thing. Working in retirement can provide more than a paycheck; it gives seniors structure, job satisfaction, and opportunities for social interaction.

Americans are feeling squeezed across the board

The reality is that the economy today is hurting Americans across the country, regardless of where one is from or how much one makes. For starters, job security is of course a grave challenge for Americans today, which may likely continue. This reality is even more stark for pre-retirees and seniors. In fact, 30% of workers over the age of 62 have recently been laid off or furloughed due to coronavirus. And 38% of workers over 65 have recently been laid off or furloughed.

Of those still working, thirty percent believe it is likely they will be laid off or have their income reduced within the next six months. Half of those currently furloughed believe they will lose their jobs or have their income cut by the Fall.

Given the current economic climate, one in ten respondents are planning to dip into their emergency savings. And one in five Americans believe they will have to draw from their 401(k). For those recently furloughed, 20% believe they will have to tap their retirement savings now. And half of those who recently lost their jobs are now planning to withdraw from their 401(k). If many withdraw, that alone could have a dramatic impact on the stock market.

Social Security beneficiaries, many of whom are dependent on their fixed income and retirement portfolios, are also feeling squeezed. Of beneficiaries today, 11% are now considering selling their home to cover their expenses. Another 10% of beneficiaries are considering refinancing their home to cover expenses today.

Of course, some Americans see an opportunity in the down economy. While over 41% are now planning to save more in their bank accounts, 21% of respondents are planning to invest more money in the stock market today.

Women remain more fiscally conservative, however. Of female respondents, 45% plan to save more today, versus 37% of males. Additionally, just 17% of women plan to buy stock today, compared to 27% of males.

But the truth is that a majority of Americans are struggling. Four in ten respondents answered they would not have the means to come up with $500 in cash today. They reported that they would either have to sell something or go to family and friends for a loan to get that kind of cash right now.

Takeaways

So much has changed in the last two months about the way we live our lives, and indeed, what life even looks like in this new reality. The human toll from the coronavirus continues to climb. Some states are reopening, while others remain closed for what seems an indefinite amount of time. Policy changes meant to ease the burden on strained businesses and struggling American citizens can feel confusing to navigate. Concern about financial scams and fraudulent spending seem to be around every corner in the wake of the pandemic. Uncertainty seems to be the only certainty.

So it is natural that many Americans are feeling at best concerned and at worst overwhelmed in thinking about and planning for their futures today. Yet that is why it is more important than ever to educate oneself on the options for retirement.

Americans who are not yet retired but whose finances have been impacted by the pandemic can use this time to review their expenses. Determine how much cash will be needed in retirement, and make any necessary adjustments to savings and portfolio asset allocations. “For those who are eligible but not yet on Social Security, while we don’t necessarily recommend taking benefits earlier, this is a good time to consider how to maximize your benefits,” says Simplywise CEO Sam Abbas. “That means understanding and calculating your options for earned benefits, spousal benefits and survivor benefits.” The best way to understand what you’re owed is to use a comprehensive Social Security calculator and checklist.

Things are changing rapidly – but staying informed, aware, and empathetic with yourself and those around you will ensure that your life today and future planning remain on track.

Methodology

Simplywise conducted its May 2020 Retirement Confidence Index online, as a random sample survey of 1,070 Americans aged 18 and above. The survey was fielded May 8-9, 2020. It was intended to explore how citizens are looking at retirement, Social Security, and savings today, particularly in light of the current crisis.