Illustrative Example

John wants to invest $20,000 and decides to use a CD ladder strategy. He splits this money among five CDs, each with an increasing term length. He invests $4,000 in a one-year CD, another $4,000 in a two-year CD, then in a three-year CD, a four-year CD, and finally a five-year CD.

When John’s one-year CD reaches its maturity date, he can choose to use that money right away or reinvest it into another five-year CD. Then, when the second-year CD reaches its maturity date, he can use it or reinvest it. He can repeat the process with each CD as they reach maturity. This means that he has a CD maturing every year. If John reinvests each year, he’ll eventually end up with 5 five-year CDs, maximizing his interest.

If John decides to reinvest his money at the end of a CD’s term length, he can vary the term length of the CD he reinvests in. He doesn’t have to split his investment up over five CDs. He can put his money into any number of CDs with varying amounts in each CD.

How does a CD ladder give John greater access to his money? Let’s say John has a CD with a maturity of one year and three more CDs with a two-year, three-year, and four-year term length. Once the shortest-term CD has reached the maturity date, he can use that money if needed while his other CDs are still maturing. When each of his CDs reaches maturity, he has the choice of using the money or reinvesting as he sees fit.

CDs can be a lucrative investment for those who want to get more out of their savings. Standard CDs may be a good option if you want to put a chunk of money away that you know you won’t need for a certain amount of time. But there are other CDs that can better work for your individual investment strategy. CD laddering is one way to maximize earnings while ensuring your money is still available to you. It also allows for flexibility and the potential to lock in higher interest rates. If you’re strategic with building your CD ladder, you can maximize earnings and have your money ready when you need it.

Types of CDs

So far in this guide, we’ve looked at how a plain vanilla CD works, but there are other types of CDs that take a step away from the traditional formula:

- Jumbo CD: A jumbo CD provides higher interest rates but requires a much higher minimum balance ($100,000 and up). The standard guidelines for a CD still apply.

- Step-up CD: In a step-up CD, your APY will automatically go up at regular intervals.

- Liquid CD: These CDs usually provide a lower rate of return, but they allow you to withdraw money during the term with little to no penalty. Liquid CDs often require a maintained minimum balance.

- Bump-up CD: With a bump-up CD, if your bank raises its APYs, you can request higher interest rates. Usually, you can only request an interest rate increase once or twice, depending on the term length. Bump-up CDs often have lower interest rates than fixed-rate CDs. Some also have greater minimum deposit requirements.

CDs and Retirement

For those approaching retirement age, CDs can be an attractive cash management strategy due to their risk characteristics and liquidity. It’s also worth considering IRA CDs, which have the risk profile but are tailored for retirement investing, as interest earned is tax-deferred. When the CD matures, investors can roll them into new CDs and will not pay taxes until withdrawing the money at retirement.

The Pros and Cons of CDs

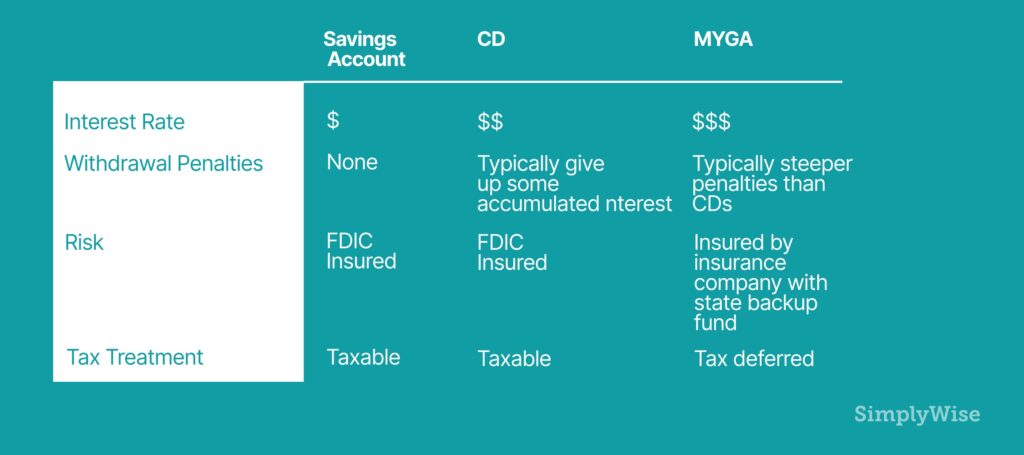

Now let’s weigh the overall pros and cons of investing in a CD. We’re going to compare a CD to a savings account and a tax-deferred annuity, the Multi-Year Guaranteed Annuity.

One major appeal of a CD is that the rate of return is higher than what you’d get in a savings account. And it’s low risk because the account is FDIC insured. But the interest rates do tend to be lower than that for a Multi-Year Guaranteed Annuity.

However, you have to keep your money locked up, often with strict penalties for taking it out early. And even though the rate of return is higher than a savings account, it’s often less than what you can get in the stock market