The US has experienced close to a 10-year bull market; since 2009, the S&P 500 has returned over 270%. When the inevitable market correction comes, which type of investors will feel the most pain? We looked at data on the finances of US households to identify three categories of investors who have the most exposure to stocks relative to their net worth and are likely to suffer the most during a correction.

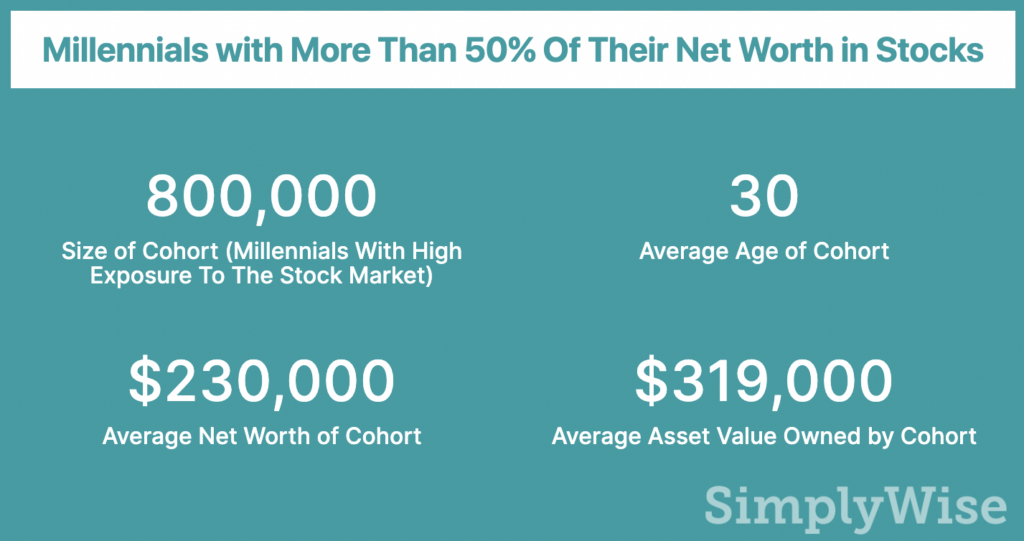

Stock ownership is typically concentrated amongst older households who have a higher net worth. The millennium population, however, does have some exposure to stocks. There are 37 million households in the US where the head of household is a millennial (younger than 40), and of these, about 5 million have some exposure to stocks through either direct stock ownership or stock funds. Of the 5 million millennials who own some stocks, roughly 400,000 have negative net worth, meaning their liabilities (student loans, credit card debt, etc.) exceed their assets. There are another 400,000 millennials who have a positive net worth, but for whom stocks make up over 50% of their net worth.

These 800,000 millennials will likely feel pain during the inevitable stock market crash as they see their net worth plummet. The good news is that this cohort is relatively young and has earning potential. While they may see the value of their stocks plummet, they have time to make the money back, assuming they are patient and keep invested in the market.

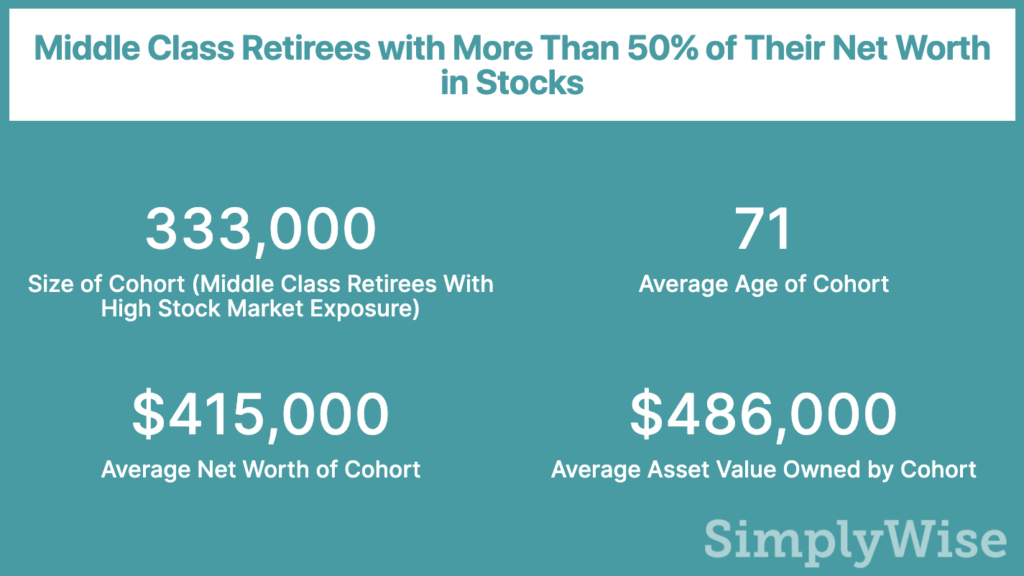

This group of people will feel the pain of a stock market decline most acutely. There are roughly 43 million households in the US where the head of household is over the age of 60. Of this group, about 35 million households have a net worth of less than 1 million dollars. These are folks who have worked a significant portion of their lives and are looking to either retire soon or have already retired. A portion of them, about 330,000, have over 50% of their net worth either directly invested in stocks or through stock funds.

Take a single data point from the survey results: this category includes a 62-year-old divorced father of one with an income of $90,000 a year and a net worth of $540,000, with $275,000 of that in a stock mutual fund. If the market drops 20%, he will likely lose about 10% of his net worth.

Investors such as these benefit massively during a long bull market as they see their net worth soar, but also stand to lose significantly when their stock market gains over several years can evaporate overnight.

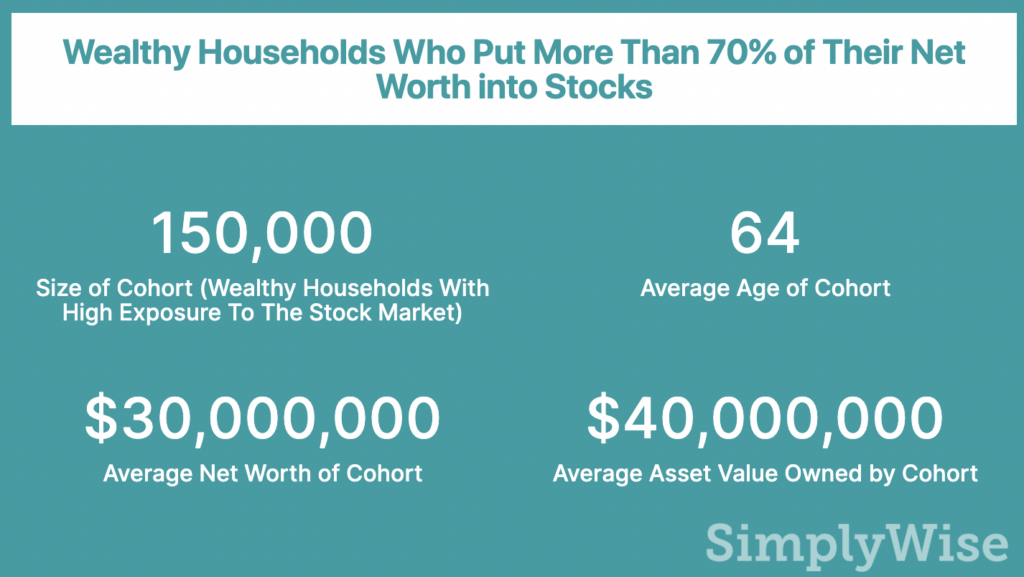

While few will have sympathy for the class of wealthy households who have a net worth of more than $1.5MM, a fraction of them (150,000) have decided to put almost all of their net worth into stocks. This demographic skews to the ultra-wealthy. The average net worth of this cohort was $30 million!

An example of this category of investor from our data is a 72-year-old with no children, with a net worth of $5.3MM, who owns $4.4MM in stock funds and $275,000 in stocks directly. That means that almost 90% of his net worth is tied to the stock market. If the market drops 20%, his net worth will drop by about $1MM. If that happens, he’ll still have enough money to live more comfortably than the entire country, but it will likely cause him some degree of pain!

Conclusion

The stock market is a great way for households to participate in the growth of the US economy and grow their wealth. However, overexposure to the stock market can cause investors to panic at the wrong time and reduce their holdings right when it is best to hold on.